What Medicare Wont Cover

Original Medicare Part A hospital insurance and Part B medical insurance offers broad coverage at a relatively low cost, but there are many potentially expensive health-care services that are not covered.

Some may be fully or partially covered by a Part C Medicare Advantage Plan, which replaces Original Medicare, or a Medigap policy, which supplements Original Medicare. Both are offered by Medicare-approved private insurers. (You cannot have both a Medicare Advantage Plan and a Medigap policy.)

Whether you are looking forward to Medicare in the future or are already covered, you should consider these potential expenses in your strategy for paying health-care expenses in retirement.

Deductibles, copays, and coinsurance. These costs can add up if you have a serious health condition, and unlike most private insurance there is no annual out-of-pocket maximum. Medicare Advantage and Medigap plans may pay all or a percentage of these costs and may include an out-of-pocket maximum.

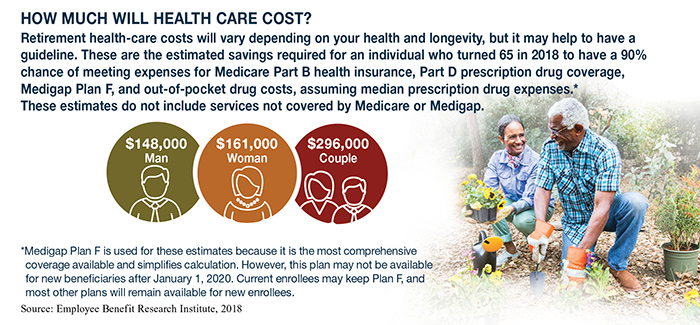

Prescription drugs. For coverage, you will need to enroll in a Part D prescription drug plan or a Medicare Advantage plan that includes drug coverage.

Dental and vision care. Original Medicare does not cover routine dental or vision care. Some Medicare Advantage and Medigap plans may offer coverage for either or both of these needs. You might also consider private dental and/or vision insurance.

Hearing care and hearing aids. Some Medicare Advantage plans may cover hearing aids and exams.

Medical care outside the United States. Original Medicare does not offer coverage outside the United States. Some Medicare Advantage and Medigap plans offer coverage for emergency care abroad. You can also purchase a private travel insurance policy.

Long-term care. Medicare does not cover custodial care in a nursing home or home health care. Part A hospital insurance does cover medically necessary stays in a certified skilled nursing facility for the first 100 days after a qualifying hospital stay of three or more days, with no out-of-pocket cost for the first 20 days, $170.50 per-day coinsurance for days 21100 (in 2024), and no coverage beyond 100 days. You may be able to purchase long-term care (LTC) insurance from private insurers.

A complete statement of coverage, including exclusions, exceptions, and limitations, is found only in the LTC insurance policy. It should be noted that LTC insurance carriers have the discretion to raise their rates and remove their products from the marketplace.